Planning to apply for a loan? Discover 5 essential tips before choosing Loan Consultancy Services. Master the Business Loan Process 2026 and grow with Growmore Finance.

Introduction: Why Your Loan Strategy Matters in 2026

Getting a loan is no longer just about filling out a form.

In 2026, the financial landscape has shifted.

Digital lending is faster, but the criteria are stricter.

Whether you are an SME owner looking to scale or a professional planning a dream home, the right preparation saves lakhs in interest.

Most people rush into a loan application and face rejection.

This guide will change that for you.

You will learn the exact steps to navigate the Business Loan Process 2026.

We will also explore how professional Loan Consultancy Services can bridge the gap between your dreams and a bank’s approval.

Let’s dive into the five pillars of a successful loan application.

1. Understanding Your Debt-to-Income Ratio

Before you ask a bank for money, you must know your capacity to repay.

Banks look at your Debt-to-Income (DTI) ratio.

This is the percentage of your monthly income that goes toward paying debts.

The Practical Use Case

Imagine a shop owner earning ₹2,00,000 per month. If they already pay ₹80,000 in existing EMIs, their DTI is 40%. Adding another loan might push them into a “high-risk” zone.

Benefits of a Low DTI

1] Faster loan approvals.

2] Power to negotiate lower interest rates.

3] Lower financial stress on your business cash flow.

Actionable Insight

Aim to keep your DTI below 35%. If it’s higher, focus on closing small credit card debts before applying for a major business or personal loan.

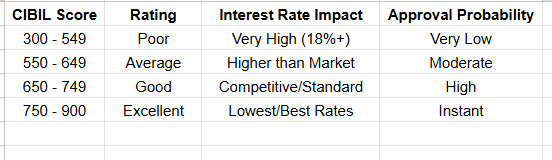

2. The Role of Credit Health: CIBIL Score Improvement Tips

Your credit score is your financial resume.

In 2026, banks are using AI-driven scoring models that look beyond just your history.

They look at your “credit behavior.”

CIBIL Score Improvement Tips for 2026

Pay on Time: Even a one-day delay can dent your score.

Credit Mix: Maintain a healthy balance of secured (Home/Car) and unsecured (Personal/Business) loans.

Limit Inquiries: Don’t apply to five banks at once; it makes you look “credit hungry.

Check for Errors: Review your credit report every quarter for mistakes.

Why it Matters

A score above 750 opens doors to the best Loan Consultancy Services and premium bank offers. Anything below 650 might lead to high-interest “subprime” loans.

3. Mastering the Business Loan Process 2026

For SME owners, the Business Loan Process 2026 has become highly documented.

Gone are the days of vague balance sheets.

The New Documentation Standard

Today, banks require:

1] GST Analytics: Your real-time sales data.

2] Cash Flow Projections: Not just what you made, but what you will make.

3] Digital Footprint: Proof of online transactions and business stability.

Practical Example

A small manufacturing unit in Gujarat needs ₹50 Lakhs for new machinery. Instead of just showing last year’s profit, they provide a 12-month projected revenue plan based on new export orders. This proactive approach ensures approval.

Actionable Insight

Consult with Loan Consultancy Services like Growmore to audit your documents before they reach the bank’s desk.

4. Choosing the Right Type of Interest Rate

Should you go for Fixed or Floating?

In 2026, market volatility is a reality.

Fixed Rates

Best for: Budget-conscious salaried professionals.

Benefit: Your EMI stays the same, regardless of market changes.

Floating Rates

Best for: Long-term Home Loans or Business Loans.

Benefit: If the RBI drops repo rates, your interest burden decreases automatically.

Actionable Insight

If you expect to close your loan early, check the prepayment penalty clause. Many “cheap” loans have hidden costs for early closure

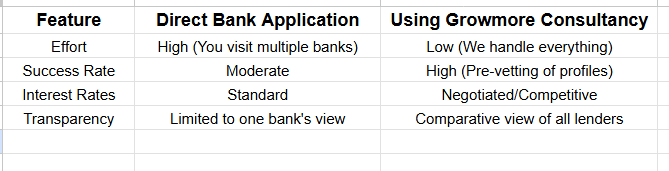

5. Why You Need Professional Loan Consultancy Services

Why do it alone when experts can do it better?

Navigating the banking maze is exhausting.

The Growmore Finance Advantage

At Growmore Finance, we don’t just “apply” for a loan. We strategize.

Bank Matching: We know which bank is “hungry” for SME loans this month.

Documentation Support: We fix the gaps in your paperwork.

Negotiation: We use our volume-based relationships to get you a better deal.

Comparison: Direct Bank Application vs. Loan Consultancy Services.

Expert Tips for SME Owners & Professionals

1] The “Buffer” Rule: Always apply for 10% more than you need to cover processing fees and initial setup costs.

2] Insurance is Key: Secure your loan with a term plan. This ensures your family or business isn’t burdened if something happens to you.

3] Automate EMIs: Set up an E-mandate. Missing an EMI in 2026 is a digital “red flag” that stays on your record for years.

https://www.rbi.org.in/commonman/Hindi/scripts/faqs.aspx?id=3558

Common Mistakes to Avoid

Hiding Existing Liabilities: Banks will find out. Honesty is the only policy.

Using Business Loans for Personal Expenses: This creates a tax nightmare and hurts business growth.

Ignoring the Fine Print: Always read the “Processing Fee” and “Foreclosure Charges” sections.

Over-leveraging: Just because you can get 1 Crore doesn’t mean you should take 1 Crore.

Is Your Loan Application Ready?

Before you hit “Apply,” check these boxes:

* Is your CIBIL score above 720?

* Are your last 6 months’ bank statements clean (no bounces)?

* Have you compared at least 3 different lenders?

* Is your ITR (Income Tax Return) filed and up to date?

* Have you consulted a Loan Consultancy Services expert?

Conclusion: Grow Your Future with Confidence

Securing a loan shouldn’t feel like a gamble.

By focusing on your DTI, maintaining your credit health, and understanding the Business Loan Process 2026, you position yourself as a “Gold Profile” borrower.

Remember, a loan is a tool.

When used correctly, it’s the fuel that drives your business expansion or secures your family’s future.

At Growmore Consultancy, we are committed to making your financial journey seamless.

Don’t let paperwork stand in the way of your progress.

Take the Next Step

Ready to scale your business or buy your dream home?