You want to scale your business.

You have the vision. You have the team. You have the market demand.

But there is one thing holding you back.

Capital.

Scaling a small or medium enterprise (SME) takes serious cash.

Whether you need to upgrade machinery, hire more staff, or manage daily working capital, cash flow is the lifeblood of your business.

Fortunately, the Government MSME Loan Scheme 2026 is designed specifically to solve this exact problem.

The government wants your business to succeed.

They are offering heavily subsidized, collateral-free credit to help you grow.

But here is the hard truth.

Most SME owners fail to secure these funds.

Why? Because the application process can feel like a maze of paperwork, portals, and banking jargon.

Not anymore.

At Growmore Finance, we believe in making business growth simple, predictable, and stress-free.

In this comprehensive guide, we will walk you exactly through the MSME Loan Online Apply 2026 process.

You will learn exactly which schemes fit your business, how to qualify, and how to get your funds disbursed in record time.

Let’s dive in.

Understanding the Government MSME Loan Scheme 2026

Before you apply, you need to understand the landscape.

The Indian government has doubled down on supporting small businesses in 2026.

They understand that SMEs are the backbone of the economy.

To stimulate growth, they have revamped their loan schemes to be faster, more digital, and highly accessible.

Explanation: A government MSME loan is a credit facility backed, subsidized, or guaranteed by state or central government bodies. Instead of begging private lenders for high-interest loans, you get access to low-cost capital.

Practical Use Case:

Imagine you own a local manufacturing unit. You just landed a massive corporate order. You need ₹15 Lakhs to buy raw materials immediately. A traditional bank might take two months and demand your house as collateral. A government-backed MSME loan can fund you in weeks, with zero collateral.

Benefits:

Zero collateral required (for specific schemes).

Lower interest rates than traditional business loans.

Longer repayment tenures.

Faster processing through digitized government portals.

Actionable Insight:

Stop looking at traditional unsecure business loans first. Always exhaust your government-backed options before accepting higher private interest rates.

👉👉👉CLICK Here —>>>business-loan-vs-msme-loan-guide

Top Collateral-free Business Loans for MSMEs

If you do not want to pledge your home, office, or personal assets, you are in luck.

The government offers phenomenal collateral-free business loans for MSMEs.

Here are the top programs you need to know for 2026.

The Mudra Loan 2026 Online Apply Process

The Pradhan Mantri Mudra Yojana (PMMY) is the most popular scheme for micro-enterprises.

It is designed to “fund the unfunded.”

Explanation:

Mudra loans offer up to ₹10 Lakhs to non-corporate, non-farm small/micro enterprises. The government guarantees these loans, meaning the bank takes on zero risk, and you put up zero collateral.

It is divided into three tiers:

Shishu: Up to ₹50,000 (For brand new startups).

Kishore: ₹50,001 to ₹5,00,000 (For buying equipment or working capital).

Tarun: ₹5,00,001 to ₹10,00,000 (For established businesses ready to scale).

Practical Use Case:

A local bakery wants to open a second location. They need ₹8 Lakhs for commercial ovens and deposit money. They apply under the “Tarun” category and secure the funding without putting their personal property on the line.

Actionable Insight:

If you need under ₹10 Lakhs, the Mudra Loan 2026 Online Apply route via the JanSamarth or Udyami Mitra portal is your absolute best starting point.

Deep Dive: CGTMSE Scheme Details

What if you need more than ₹10 Lakhs?

This is where the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) comes in.

Explanation:

The CGTMSE Scheme details for 2026 are incredibly lucrative for growing SMEs. The government provides a credit guarantee of up to ₹5 Crores to the lending institution.

If your business defaults (which we hope it doesn’t), the government pays the bank up to 85% of the loan amount.

Because the bank’s risk is covered, they are happy to lend to you without collateral.

Practical Use Case:

A tech startup needs ₹2 Crores to build a new software facility and hire 50 developers. They lack physical assets to pledge. Using the CGTMSE scheme, they secure a term loan based purely on their strong business plan and cash flow projections.

Benefits:

Massive capital access (up to ₹5 Crores).

Purely cash-flow based lending.

Available for both term loans and working capital limits.

Actionable Insight:

To get a CGTMSE loan, your project report must be flawless. Banks rely entirely on your financial projections to approve this loan.

https://www.cgtmse.in/

Prime Minister’s Employment Generation Programme (PMEGP)

PMEGP is a credit-linked subsidy scheme.

This means the government actually pays off a portion of your loan.

Explanation:

For new manufacturing units (up to ₹50 Lakhs) and service units (up to ₹20 Lakhs), the government provides a margin money subsidy ranging from 15% to 35%.

Practical Use Case:

You start a rural manufacturing unit taking a ₹50 Lakh loan. The government provides a 35% subsidy (₹17.5 Lakhs). You only ever have to repay ₹32.5 Lakhs.

Actionable Insight:

Only apply for PMEGP if you are setting up a brand new project. It is not for existing business operations.

Ready to Scale Your Business?

Stop struggling with working capital. Let the experts at Growmore Finance handle your loan application from start to finish.

👉👉👉CLICK Here —>>> Book Your Free Funding Strategy Apply Today

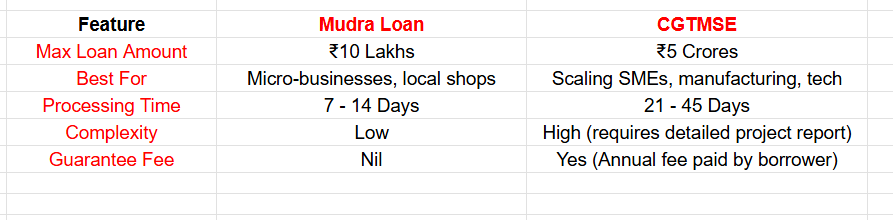

Mudra vs. CGTMSE: Which is Right for You?

Not sure which scheme fits your business?

Let’s break it down simply.

Here is how the top collateral-free business loans for MSMEs compare.

Actionable Insight:

Match your funding need to the exact scheme. Do not apply for CGTMSE if you only need ₹5 Lakhs. It will overcomplicate your life.

Cracking the Code: Eligibility for MSME Loan 2026

Banks do not hand out money to just anyone.

You need to prove you are a safe bet.

The eligibility for MSME loan 2026 is strict, but highly logical. Here is exactly what lenders look for.

1. Udyam Registration (Non-Negotiable)

You must be officially registered as an MSME. The Udyam registration is a free, digital certificate provided by the government. Without it, you do not exist in the eyes of these schemes.

2. Business Vintage

While Mudra covers startups, most high-value loans (like CGTMSE) require at least 1 to 3 years of profitable business vintage.

3. The Magic Credit Score

Your CIBIL score is your financial resume.

Personal CIBIL: Minimum 700+.

Commercial CIBIL (CMR): Must show a strong repayment history.

4. Financial Health

Banks want to see rising revenue. They will scrutinize your last 2 years of ITRs (Income Tax Returns) and GST returns.

Practical Use Case:

A retail owner applies for a loan but gets rejected. Why? Her GST returns showed ₹50 Lakhs in sales, but her ITR only showed ₹20 Lakhs. Mismatched financials are an instant red flag.

Actionable Insight:

Before starting your MSME Loan Online Apply 2026, sit with your CA. Ensure your GST, ITR, and Bank Statements tell the exact same story.

MSME Loan Interest Rates 2026: What to Expect

Capital is not free.

But government schemes make it highly affordable.

Understanding the MSME loan interest rates 2026 helps you calculate your true cost of growth.

Explanation:

Interest rates for MSME loans are usually linked to the RBI’s Repo Rate or the bank’s Marginal Cost of Funds Based Lending Rate (MCLR).

For 2026, you can generally expect:

Mudra Loans: 8.5% to 11.5% p.a.

CGTMSE Loans: 9.0% to 12.0% p.a.

Stand-Up India: 9.5% to 10.5% p.a.

Benefits of Government Rates:

Private NBFCs (Non-Banking Financial Companies) often charge 16% to 24% for unsecured business loans. By securing a government-backed loan at 9%, you save lakhs in interest payments every single year.

Actionable Insight:

Always negotiate the processing fee. While interest rates are largely fixed based on your risk profile, bank processing fees (usually 1% to 2%) can often be negotiated down by a smart founder.

how-to-calculate-business-loan-emi

Want the Latest Interest Rate Updates Delivered to Your Inbox?

Stay ahead of the market. Join 10,000+ smart founders getting weekly financial insights.

👉👉👉CLICK Here —>>>Apply to the Growmore Finance

Step-by-Step: MSME Loan Online Apply 2026

It is time to take action.

The days of standing in bank queues with thick files are over. The government has digitized the ecosystem.

Here is your exact MSME Loan Online Apply 2026 blueprint.

Step 1: Register on the Udyam Portal

Go to the official Udyam Registration portal. Keep your Aadhaar and PAN card ready. Fill out the details about your business activity. It takes 10 minutes, and the certificate is generated instantly.

Step 2: Prepare Your Digital Arsenal

Before logging into any loan portal, gather your PDF documents.

Last 3 years ITR.

Last 12 months GST returns.

Last 12 months Bank Statements (Current Account).

KYC documents (Aadhaar, PAN of promoters).

Detailed Project Report (if applying for >₹10 Lakhs).

Step 3: Choose Your Portal

The government operates centralized marketplaces where your application goes to multiple banks at once.

👉CLICK Here ->>JanSamarth Portal: Best for Mudra and Subsidy schemes.

👉CLICK Here ->>Udyami Mitra: Excellent for matching with preferred public and private sector banks.

👉CLICK Here ->>PSB Loans in 59 Minutes: Best for instant in-principle approvals for working capital.

Step 4: Fill the Application Data

Upload your GST and bank statements. The AI-driven portals will instantly analyze your cash flow and tell you how much you are eligible for.

Step 5: Select Your Bank

The portal will show you offers from various banks (e.g., SBI, HDFC, Bank of Baroda). Compare their interest rates and select the best fit.

Step 6: In-Principle Approval & Physical Verification

You will receive a digital “In-Principle Approval.” The selected bank will then contact you. They may visit your business premises to verify operations before final disbursal.

Actionable Insight:

Use the “PSB Loans in 59 Minutes” portal if you have clean, flawless digital records. It pulls data directly from the GST portal and Income Tax portal, saving you hours of manual data entry.

5–Common Mistakes When Applying for Business Loans

Even with a great business, your application can be thrown in the trash.

Avoid these fatal errors.

1. Bouncing Cheques: Banks check your last 12 months’ bank statements. If they see EMI bounces or cheque returns, your application is dead on arrival.

2. Mixing Personal and Business Funds:

Do not buy groceries from your current account. Do not deposit personal cash into the business account without proper accounting. Keep it clean.

3. Applying to Multiple Banks Simultaneously:

Every time a bank checks your CIBIL score, it registers a “Hard Inquiry.” Too many hard inquiries drop your score and make you look desperate for cash. Use the centralized portals instead.

4. Poor Project Reports:

For CGTMSE loans, your project report is everything. If your projected revenue growth looks wildly unrealistic, the credit manager will reject it.

5. Ignoring Existing Debt:

If your current EMI obligations are already eating up 60% of your profits, no bank will give you another loan.

Actionable Insight:

Do a “mock audit” of your own bank statements before applying. Highlight any irregularities and have a logical explanation ready for the bank manager.

Expert Tips from Growmore Finance to Speed Up Approval

Want to skip the line?

Here is how the pros get loans disbursed in 14 days instead of 45.

Focus on Banking Hygiene

Maintain a high Average Bank Balance (ABB). Banks love businesses that keep cash in their current accounts.

Build a Relationship with the Branch Manager

Portals get you the approval, but branch managers do the disbursal. Visit the branch, shake hands, and explain your business vision clearly.

Clear Statutory Dues

Ensure all your GST, TDS, and PF payments are up to date. Government banks will instantly reject you if you owe tax money.

Leverage Growmore Finance

Why do it yourself? Working with an expert financial consultancy ensures your file is perfect the first time. We know exactly what credit managers want to see.

Your Ultimate MSME Loan Application Checklist

Do not hit “Submit” until you have checked every box on this list.

[✔️ ] Udyam Registration Certificate downloaded.

[✔️ ] Personal and Business PAN Cards ready.

[✔️ ] CIBIL score checked (Must be 700+).

[✔️ ] Last 3 years ITRs filed and downloaded.

[✔️ ] Last 12 months GST returns downloaded.

[✔️ ] Last 12 months Current Account statements in PDF.

[✔️ ] Business Plan / Project Report prepared (for loans >₹10L).

[✔️ ] Proof of business address (Utility bill, Rent agreement).

[✔️ ] Projected financials for the next 2 years signed by CA.

Conclusion & Next Steps

Securing capital does not have to be a nightmare.

The Government MSME Loan Scheme 2026 is incredibly well-structured, offering phenomenal opportunities for high-growth SMEs.

By understanding the CGTMSE Scheme details, knowing the exact eligibility for MSME loan 2026, and perfectly executing the MSME Loan Online Apply 2026 process, you put your business on the fast track to success.

Key Takeaways:

- Always seek collateral-free business loans for MSMEs first.

2) Ensure your GST, ITR, and Bank Statements perfectly align.

3) Use digital portals like JanSamarth for faster processing.

4) Keep your CIBIL score pristine.

At Growmore Finance, we are dedicated to turning your growth vision into reality. Capital is waiting for you. It is time to go get it.

Ready to get funded?

Contact Growmore Finance today. Let our experts structure your file, secure the best MSME loan interest rates 2026, and get the capital directly into your bank account.

👉CLICK Here ->>Contact Growmore Finance for a Free Consultation