1. MSME Loans: Government-Backed Growth

MSME loans are designed for accessibility. If your business is registered on the Udyam portal, you unlock several specific schemes:

PMMY (Mudra Loan): Best for micro-units and startups.

Shishu: Up to ₹50,000.

Kishore: Up to ₹5 Lakh.

Tarun: Up to ₹10 Lakh (recently extended up to ₹20 Lakh for specific cases).

CGTMSE: Provides a credit guarantee to banks, allowing you to secure up to ₹5 Crore without pledging personal assets or property.

PMEGP: A subsidy-linked scheme (15%–35% subsidy) focused on generating employment in manufacturing and service sectors.

SIDBI SMILE: Soft loans for modernization and technology upgrades with a moratorium period (grace period) on principal repayment.

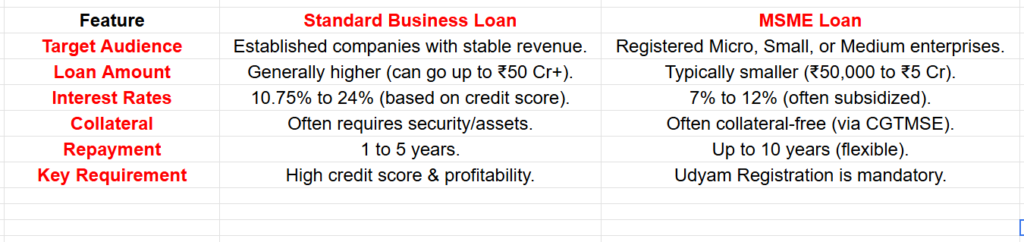

2. Business Loans: Flexibility for Scaling

Standard business loans are better suited for “Large” enterprises or established businesses that do not fit the MSME turnover criteria (above ₹250 Cr).

Speed: Private banks and NBFCs often process these faster if financials are strong.

Usage: Greater flexibility in how funds are used (e.g., high-value international expansion).

Pre-payment: Often carry specific charges for closing the loan early, unlike some government MSME schemes.

Eligibility Checklist (2026 Standards)

To qualify for the best rates in the current market, lenders typically look for:

Udyam Registration: The “Golden Ticket” for MSME benefits.

CIBIL Score: A score of 700+ is ideal, though some NBFCs accept 650+ with strong cash flow.

Business Vintage: At least 1 to 3 years of active operations for existing businesses.

GST Compliance: Regular GST filings are now a primary indicator of “trust” for lenders.

Which should you choose?

Choose an MSME Loan if: You are a small/medium manufacturer or service provider looking for the lowest possible interest rate and do not want to provide collateral.

Choose a Business Loan if: You need a massive capital infusion (e.g., ₹20 Cr+) quickly and have the assets or high turnover to back it up.