The biggest financial debate of 2026 is here.

Should you pay rent and keep your cash liquid?

Or should you take a home loan and build a lifelong asset?

If you are a salaried professional looking for stability, the answer feels obvious.

But if you are an SME owner who needs working capital to scale, blocking cash in real estate can stall your business growth.

Welcome to Growmore Finance’s definitive guide on rented home vs housing loan pros and cons India.

In this guide, we break down the exact numbers, tax laws, and market realities of 2026.

You will learn exactly how to balance your personal wealth and business growth without making costly mistakes.

Let’s dive in.

Rent vs EMI Which is Better in India: The 2026 Reality Check

The Indian real estate market has shifted dramatically.

With the RBI holding the repo rate steady at 5.25% in early 2026, the cost of borrowing has stabilized.

Current home loan interest rates hover around 7.10% to 7.50% at major banks.

Meanwhile, urban rental yields remain stubbornly low at 2% to 3%.

So, rent vs EMI which is better in India right now?

The answer depends entirely on your opportunity cost.

If your business generates a 15% return on capital, renting makes more sense.

If you are a salaried employee looking for forced savings, paying an EMI builds a powerful asset.

Let’s look at the exact advantages and disadvantages of both sides.

Benefits of Buying a House in India (The “Buy” Argument)

Owning a home is more than an emotional milestone. It is a financial fortress.

Here are the top benefits of buying a house in India:

1. Asset Creation & Capital Appreciation

Every EMI you pay increases your equity. Rent, on the other hand, makes your landlord rich. Historically, property appreciation rates in Indian cities like Pune, Hyderabad, and Ahmedabad have consistently outpaced inflation.

2. Collateral for Future Business Loans

This is a game-changer for SME owners. A self-owned property can be pledged for a Loan Against Property (LAP). This unlocks massive working capital or machinery financing for your business at much lower interest rates than unsecured loans.

3. Unmatched Emotional Security

No more forced evictions. No more asking for permission to paint a wall. You are the boss of your own space.

Click Here👉👉 business-loans-against-property-sme-guide

The Hidden Downsides of Buying (Cons of a Home Loan)

Before you sign that 20-year loan agreement, consider the risks.

1. The Down Payment Trap

Buying a ₹1 Crore house requires at least ₹20 Lakh in upfront cash. For a startup founder, that ₹20 Lakh could have been used to double business revenue.

2. Heavy Interest Outflow

In the first 5 to 7 years of a home loan, almost 80% of your EMI goes entirely toward interest. You build very little actual ownership in the initial years.

3. High Maintenance Costs

When the roof leaks, you pay for it. The maintenance costs of owned property vs rented properties are significantly higher because owners bear structural and long-term repair costs.

The Upside of Renting: Ultimate Flexibility

Renting is not “throwing money away.” It is paying for flexibility.

1. Preserving Liquidity for Growth

Instead of a heavy down payment, you keep your cash liquid. You can use this capital for business expansion or high-yield investments. When comparing real estate investment vs stocks India, equity markets historically offer higher liquidity and often better annualized returns.

2. Upgrading Lifestyle Quickly

You can rent a luxury apartment in a prime location for a fraction of what it would cost to buy an equivalent property.

3. Zero Maintenance Headaches

Property tax? Major plumbing issues? Society repair funds? That is the landlord’s problem, not yours.

The Dark Side of Renting (Cons of Rented Homes)

Renting is convenient, but it has serious long-term flaws.

1. Rising Rental Costs

Your EMI stays largely predictable. Your rent will increase by 5% to 10% every single year.

2. No Asset Creation

After 15 years of paying ₹40,000 in monthly rent, you own zero percent of the property.

3. Lack of Control

Landlords can terminate your lease, restrict pets, or hike the rent unpredictably. This instability is tough on growing families.

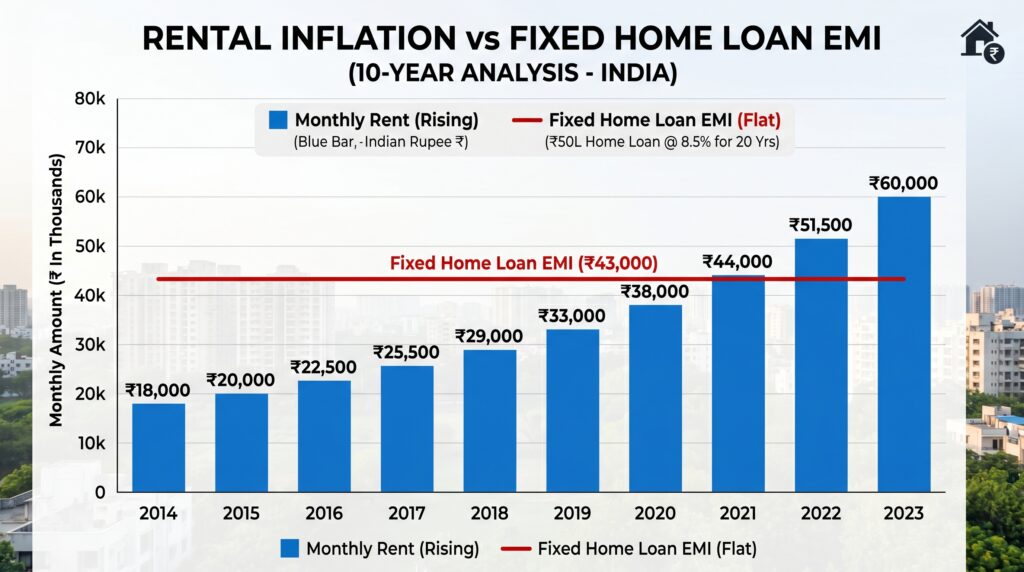

Home Loan Interest Rates vs Monthly Rent (The Numbers Game)

Let’s look at the hard data for 2026.

Assume a property costs ₹75 Lakh. The average rent for this property will be around ₹20,000 per month.

If you take a home loan of ₹60 Lakh at 7.25% for 20 years, your EMI will be roughly ₹47,000.

Home loan interest rates vs monthly rent show a massive gap in monthly cash outflow.

Your EMI is more than double the rent. However, after 20 years, the renter has nothing. The buyer owns a property likely worth over ₹2 Crores.

Actionable Insight: If your business ROI is higher than 12%, rent the house and invest the difference into your SME. If you lack business investment avenues, buy the house to build wealth.

Tax Benefits on Home Loan in India (Section 80C & 24b) Explained

Taxes can completely change the “Rent vs Buy” math.

Here is how tax benefits on home loan in India (Section 80C & 24b) work in the 2026 tax landscape:

The Old Tax Regime Edge

If you opt for the Old Tax Regime, buying a house is highly rewarding.

Section 80C: Claim up to ₹1.5 Lakh per year on your principal repayment.

Section 24(b): Claim up to ₹2 Lakh per year on your interest payment for a self-occupied property.

The New Tax Regime Reality

The New Tax Regime (default for FY 2025-26/AY 2026-27) removes these deductions for self-occupied properties. However, if you buy a property and let it out on rent, you can still deduct interest paid from your rental income.

(Always consult with your Growmore Finance advisor to structure your taxes effectively!)

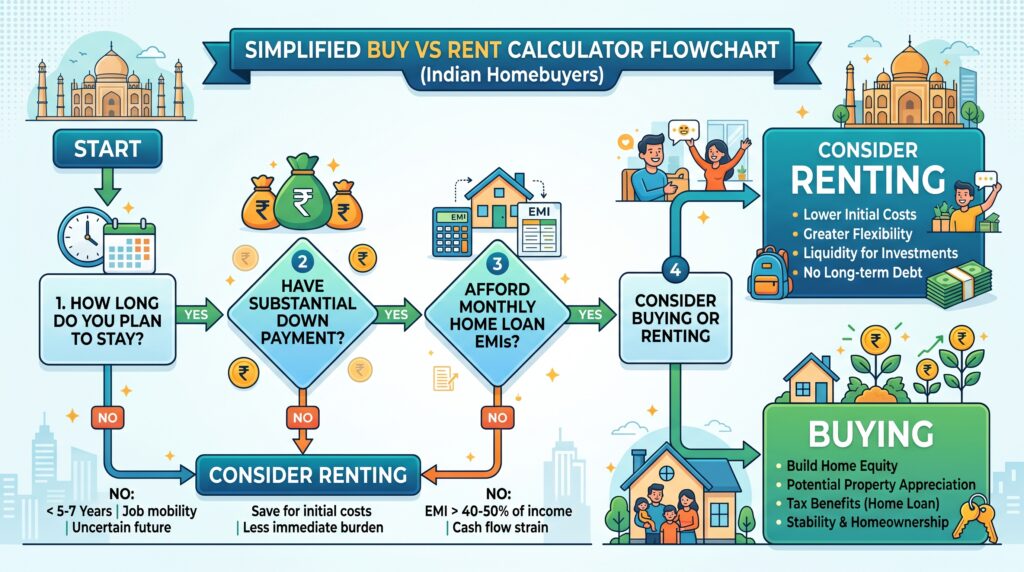

Buy vs Rent Calculator India 2026: The 5% Rule

Still confused? Use this mental Buy vs Rent calculator India 2026 framework.

Calculate the total annual rent of the house you want to live in. Divide that number by the total cost of the house.

If the rental yield is under 3%, renting makes financial sense.

If the rental yield is over 4.5% to 5%, buying is the superior choice.

Another trick is the “15-Year Rule.” If you plan to live in the same city and the same house for at least 10 to 15 years, buying always wins out against renting.

Government Support: PMAY Benefits and Affordable Housing

If you are buying your first home, the government wants to help.

Look into PMAY (Pradhan Mantri Awas Yojana) benefits. Though specific subsidy slabs vary by income group, they drastically reduce the total interest burden for first-time buyers.

Additionally, state-specific affordable housing schemes in Gujarat/Maharashtra offer reduced stamp duty and registration fee waivers.

This brings down your upfront acquisition cost significantly, making the decision to buy much easier for working professionals.

Expert Tips: Growmore Finance’s Strategic Advice

At Growmore Finance, we advise thousands of SME owners and professionals. Here is our blueprint:

For the SME Owner: Do not drain your working capital for a house down payment. Scale your business first. Rent a good home, grow your revenue, and buy a house later using business dividends.

For the Salaried Professional: Buy a house early in your career. Your income is highly stable, and the forced discipline of an EMI will build your biggest retirement asset.

For the Smart Investor: Buy a commercial property for your business, and rent your residential home. Commercial real estate yields 6-8%, paying for your rent effortlessly.

Common Mistakes to Avoid

Avoid these massive financial blunders in 2026:👇👇👇

Ignoring Job Mobility: Buying a home when your job requires moving cities every 3 years.

Stretching the Budget: Taking an EMI that is more than 40% of your in-hand monthly salary.

Forgetting Hidden Costs: Ignoring interior costs, registration, and brokerage when calculating the property price.

Comparing EMI directly to Rent: EMI includes principal (wealth creation) and interest (expense). Rent is purely an expense.

The Ultimate Checklist for Property Buyers

Before you make a decision, check off these boxes:

[✔️] Checked your CIBIL score (Aim for 750+ for the lowest interest rates).

[✔️] Compared the exact rented home vs housing loan pros and cons India for your specific city.

[✔️] Calculated the 20-year opportunity cost of your down payment.

[✔️] Consulted with a debt restructuring expert if you have existing business loans.

Conclusion & Next Steps

Deciding between renting and buying is the biggest financial choice you will make this decade.

To summarize the rented home vs housing loan pros and cons India: Buying offers security, asset creation, and business collateral. Renting offers high liquidity, ultimate flexibility, and zero maintenance.

There is no one-size-fits-all answer. Your choice must align with your business goals, career trajectory, and cash flow needs.

Are you an SME owner looking to balance property investment with working capital? Or a salaried professional trying to navigate home loan documentation?

Growmore Finance is here to simplify your journey.

Take Action Today!

Want to find the best home loan rates or restructure your business debt? Talk to our financial experts today and secure the funding you deserve.

Click Here👉👉 Coll to 7567009947 Book Your Free Financial Strategy Session with Growmore Finance

Love this guide?

Subscribe to our blog for weekly insights on business loans, tax-saving tips, and wealth creation strategies!

Click Here👉👉 Subscribe to the Growmore Finance Newsletter