You want to scale your business.

You need faster production, better quality, and bigger margins.

But heavy equipment costs serious money.

Upgrading your workshop or factory shouldn’t drain your working capital.

That is where a machinery loan without security & with security becomes your ultimate growth tool.

In 2026, the financial landscape has shifted. Lenders are more flexible. Approvals are faster.

Whether you are a local manufacturer needing a CNC machine or an SME owner upgrading your packaging line, you have options.

In this comprehensive guide, we will break down exactly how to secure the funding you need.

You will learn the difference between secured and collateral-free options.

You will discover exactly what it takes to get approved quickly.

Let’s dive in.

1. Understanding the Machinery Loan Without Security & With Security

Funding your equipment upgrades falls into two main categories.

You can pledge assets, or you can leverage your business’s financial health.

Choosing the right path determines your interest rates, loan limits, and approval speed.

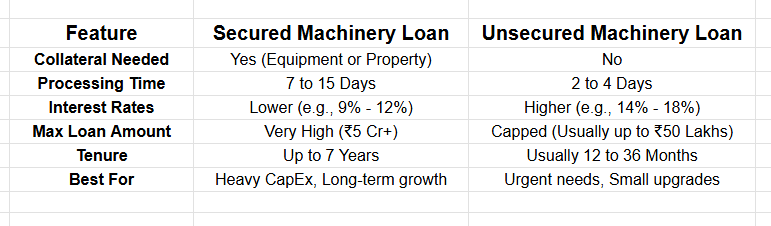

What is a Secured Machinery Loan?

A secured loan requires collateral.

Usually, the machinery you are purchasing acts as the security itself (hypothecation).

Sometimes, lenders may ask for residential or commercial property as additional backing.

Practical Use Case: A textile unit in Surat wants to import heavy water-jet looms worth ₹2 Crores. Because the loan amount is massive, the bank secures the loan against the new machinery and a factory plot.

Benefits:

Lowest possible interest rates.

Higher loan amounts (up to ₹5 Crores or more).

Longer repayment tenures (up to 7 years).

Actionable Insight: Always opt for a secured loan if you are making a massive capital expenditure (CapEx) that will take years to generate a return on investment (ROI).

What is an Unsecured Machinery Loan?

This is a pure cash flow-based loan.

You do not pledge any property. You do not hypothecate the equipment.

The lender approves you based entirely on your GST returns, bank statements, and credit score.

Practical Use Case: A small bakery wants to buy a new commercial rotary oven for ₹8 Lakhs. They need the machine installed next week to handle a huge festive order. They opt for an unsecured loan for immediate disbursement.

Benefits:

Zero collateral required.

Lightning-fast processing (often 48 to 72 hours).

Minimal documentation.

Actionable Insight: Use unsecured loans for urgent, smaller ticket-size equipment purchases (under ₹50 Lakhs) where speed is your top priority.

(business-loan-documents-guide)

2. The Rise of the Collateral-Free Machinery Loan 2026

The market is changing rapidly.

Previously, getting a business loan without pledging property was a nightmare.

Not anymore.

The collateral-free machinery loan 2026 landscape is driven by data and AI.

Lenders now use your digital footprint to assess risk.

They look at your monthly GST filings.

They analyze your bank statement transactions.

They check your Bureau score.

If your cash flow is strong, you get the money. It is that simple.

Why This Matters for SMEs

Small business owners often lack hard assets like real estate.

But they have strong daily sales.

A collateral-free loan bridges this gap perfectly.

Benefits:

Protects your personal assets.

Keeps the machinery entirely in your name from day one.

Allows you to move fast on market opportunities.

Actionable Insight: Keep your current account clean. Avoid bounced cheques and maintain a healthy minimum balance to easily qualify for collateral-free options.

3. Deep Dive: Machinery Loan for Manufacturing Units

Manufacturing is the backbone of the economy.

But it is also incredibly capital-intensive.

A specialized machinery loan for manufacturing units is tailored to these exact challenges.

How It Works

These loans often come with structured repayment plans.

Lenders understand that new machinery takes time to install, calibrate, and start producing revenue.

Therefore, they often offer a “moratorium period.”

This means you might only pay interest for the first 3 to 6 months while the machine is being set up.

Practical Use Case: A plastic injection molding business buys a new hydraulic press. The machine takes two months to arrive and one month to install. The lender offers a 3-month moratorium on principal payments.

Benefits:

Matches your cash flow cycle.

Prevents financial strain during setup.

Covers not just the machine, but often transit insurance and installation costs.

Actionable Insight: When negotiating with a lender, always ask if they cover the “landed cost” of the machinery, which includes shipping and taxes, not just the base price.

(Click Hear —->> High-authority resource on global manufacturing equipment trends)

4. Decoding MSME Machinery Loan Eligibility

You found the perfect machine.

Now, you need to know if you qualify for the funds.

Understanding MSME machinery loan eligibility saves you time and prevents loan rejections.

While every lender is different, the core criteria remain the same.

The Standard Eligibility Checklist

Here is what banks and NBFCs look for in 2026.

- Business Vintage: Your business must be operational for at least 2 to 3 years.

- Turnover: Minimum annual turnover requirements (usually starting at ₹40 Lakhs to ₹1 Crore, depending on the loan size).

- Profitability: Your business must show a net profit for the last 1 to 2 financial years.

- Credit Score: A CIBIL score of 700 or above is non-negotiable for unsecured loans.

- Registration: You must have a valid Udyam Registration (MSME certificate).

Why Your Udyam Certificate is Your Golden Ticket

Registering as an MSME unlocks government subsidy schemes.

Schemes like the Credit Linked Capital Subsidy Scheme (CLCSS) can significantly reduce your financial burden.

Actionable Insight: Before applying for any loan, ensure your Udyam certificate is updated with your correct business activities and linked to your current address.

5. Secured vs. Unsecured: The Ultimate Comparison

Which path is right for you?

The Verdict: If you have time and want the cheapest money, go secured. If you need a competitive edge right now and have strong cash flow, go unsecured.

[Image: {Infographic showing scales weighing secured vs unsecured machinery loans}]

Ready to Scale Your Operations? Stop letting outdated equipment hold your business back. Growmore Finance Services provides customized financing solutions designed specifically for ambitious SMEs.

[Get Your Free Loan Assessment Today<<<—Click Hear]

6. Real-World Use Cases

Let’s look at how businesses are actually using these loans.

Scenario A: The Auto Ancillary Startup

Need: Two new CNC milling machines.

Choice: Secured machinery loan.

Result: Hypothecated the machines. Secured an 8.5% interest rate over 5 years. Scaled production by 300%.

Scenario B: The Corporate Professional Turned Entrepreneur

Need: Packaging equipment for a new cloud kitchen.

Choice: Collateral-free machinery loan 2026.

Result: Used excellent personal CIBIL score and initial business cash flow. Got ₹15 Lakhs in 48 hours without pledging personal assets.

Actionable Insight: Match the lifespan of the machine to the tenure of the loan. Don’t take a 5-year loan on a piece of technology that will be obsolete in 3 years.

7. Step-by-Step Application Process

Getting a machinery loan without security & with security doesn’t have to be complicated.

Follow this streamlined process.

Step 1: Get the Proforma Invoice

Lenders need to know exactly what you are buying. Ask your machinery supplier for a detailed quotation or proforma invoice.

Step 2: Gather Your Financials

Compile your last 12 months of bank statements. Download your last 2 years of ITR and Audited Balance Sheets. Keep your GST returns (GSTR-3B) handy.

Step 3: Choose Your Lender

Approach banks for lower rates, or NBFCs for higher flexibility and speed. Consult with financial experts to find the right fit.

Step 4: Submit and Wait for Assessment

The lender will evaluate your Debt Service Coverage Ratio (DSCR). This simply means they check if your profit is enough to pay the new EMI.

Step 5: Sanction and Disbursement

Once approved, the lender usually pays the machinery supplier directly. You receive the machine, and your EMI schedule begins.

8. How to Choose the Right Financing Partner

Not all lenders are created equal.

You need a partner who understands your industry.

Look for these three things:

Industry Expertise: Do they understand manufacturing cycles?

Hidden Charges: Read the fine print. Look out for high processing fees or pre-closure penalties.

Speed of Execution: In business, time is money. Slow banks cost you lost orders.

Actionable Insight: Always negotiate the processing fee. While interest rates might be fixed, processing fees (usually 1% to 2%) are highly negotiable.

9. Expert Tips for Instant Loan Approval

Want to skip the line and get your funds faster?

Apply these insider strategies.

Boost Your Bank Balance: Maintain an Average Bank Balance (ABB) that is at least twice your expected EMI amount for 3 months prior to applying.

Clear Old Debts: Close small, lingering personal loans or credit card EMIs to improve your debt-to-income ratio.

Perfect Your Pitch: Be ready to explain exactly how this new machine will increase your monthly revenue. Lenders love clear business plans.

Keep Statutory Dues Clear: Ensure your GST, TDS, and PF payments are strictly up to date. Defaulters face instant rejection.

10. Common Mistakes to Avoid

Many SME owners sabotage their own applications.

Don’t make these critical errors.

Mistake 1: Applying to Multiple Banks Simultaneously Every time a bank checks your CIBIL, it leaves a “hard inquiry.” Too many inquiries drop your score and make you look desperate for credit.

Mistake 2: Overborrowing Just because you are eligible for ₹50 Lakhs doesn’t mean you should take it. Borrow only what the machine costs plus essential installation expenses.

Mistake 3: Mixing Personal and Business Finances Lenders hate seeing personal grocery bills on a current account statement. Keep them strictly separate to prove professional financial management.

11. SME Business Growth Strategies (Bonus Section)

A loan is just fuel. You still have to drive the car.

Once you secure your machinery loan for manufacturing units, maximize its value.

Run Double Shifts: If you bought the machine, make it work. Train a night shift crew to double your output and pay off the loan faster.

Market the Upgrade: Tell your clients you have upgraded your technology. Use it as a selling point to secure bigger, higher-paying contracts.

Claim Depreciation: Consult your CA. Machinery depreciation is a massive tax shield. Use it to lower your corporate tax liability at the end of the year.

12. Document Readiness Checklist

Treat this as your ultimate pre-flight checklist.

Have these ready before you approach any lender:

(1) KYC Documents (Aadhaar, PAN of Promoters).

(2) Business KYC (GST Certificate, Udyam Registration, Shop Act).

(3) Proforma Invoice of the machinery.

(4) Last 12 months’ Current Account statements.

(5) Last 3 years’ ITR with Computation of Income.

(6) Audited Balance Sheet and P&L statements.

(7) Repayment Track Record (RTR) of any existing loans.

Being organized cuts your processing time in half

Conclusion

Securing a machinery loan without security & with security is the most effective way to modernize your business in 2026.

You no longer have to drain your cash reserves to upgrade your infrastructure.

Whether you choose a collateral-free path for speed or a secured route for massive scale, the capital is out there waiting for you.

Understand your MSME eligibility. Prepare your documentation perfectly. Choose a financing partner that aligns with your vision.

The right equipment will pay for itself. You just need to take the first step.

Ready to transform your manufacturing unit or local business?

Don’t navigate the complex banking system alone.

Let the experts at Growmore Finance Services secure the best interest rates and fastest approvals for your business.

[Click Hear —->>Contact Growmore Finance Services Now for a Free Consultation]